Every initiative faces uncertainty. Even the most detailed plans encounter unexpected hurdles. Effective project risk management is not about predicting the future with absolute certainty; it is about preparing for possibilities. By identifying potential issues early, teams can reduce negative impacts and seize opportunities. This guide outlines a systematic approach to risk management, helping you navigate complexity with confidence.

🧐 Understanding the Core of Project Risk

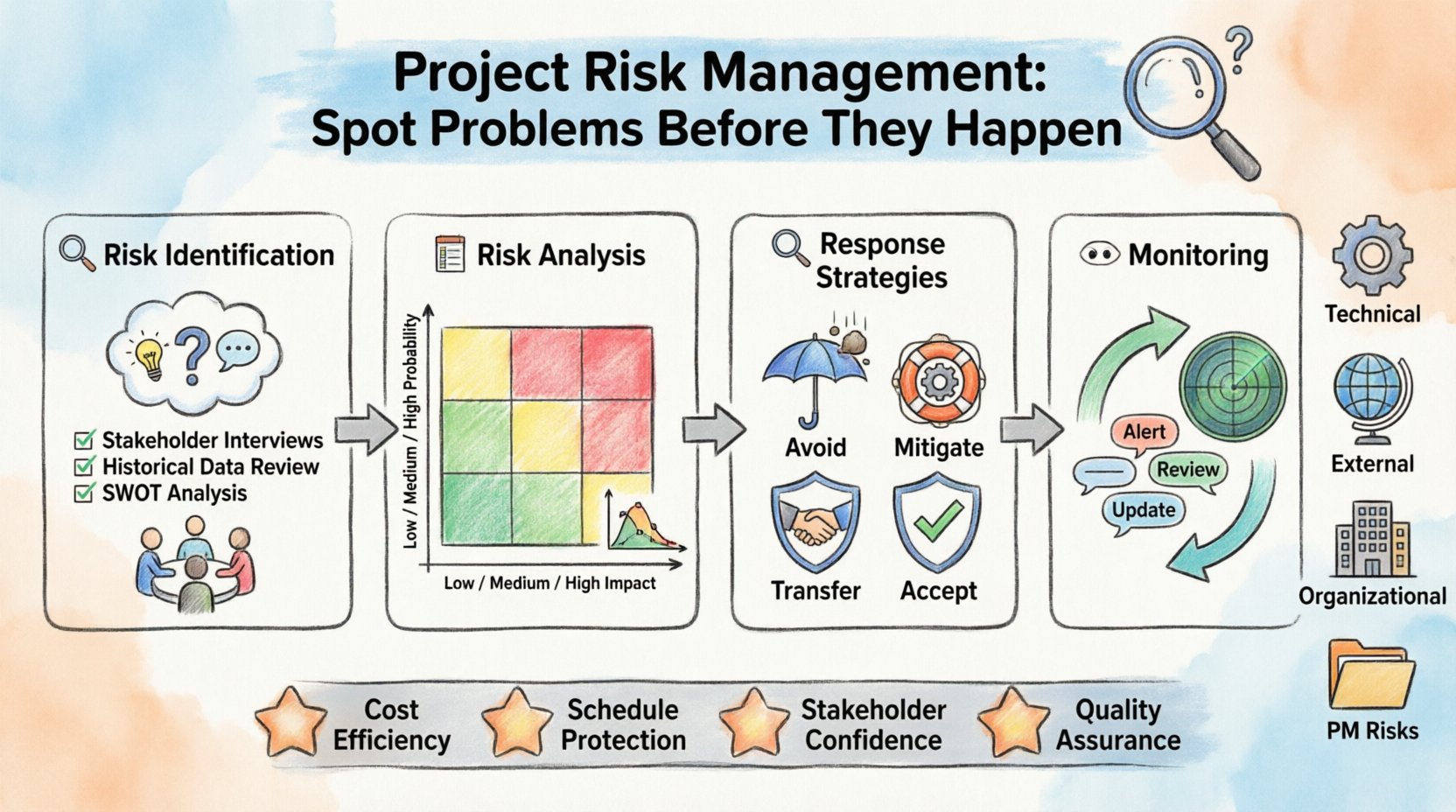

Project risk refers to an uncertain event or condition that, if it occurs, has a positive or negative effect on one or more project objectives. These objectives typically include scope, schedule, cost, and quality. Ignoring risk is a gamble; managing it is a discipline.

Many project managers focus heavily on tasks and deadlines. While important, these elements do not account for the variables that lie outside the immediate workflow. Risk management provides a framework to address these variables proactively.

Why Proactive Management Matters

Cost Efficiency: Addressing a risk early costs significantly less than fixing a failure later.

Schedule Protection: Anticipating delays allows for buffer allocation without panic.

Stakeholder Confidence: Transparent risk handling builds trust with sponsors and clients.

Quality Assurance: Identifying technical risks prevents defects from reaching the final deliverable.

🌍 Types of Project Risks

Risks vary by industry and project type. Categorizing them helps in creating a comprehensive risk register. Below are common categories you should consider during the planning phase.

Risk Category | Description | Examples |

|---|---|---|

Technical Risks | Issues related to the technology, architecture, or deliverables. | Unproven technology, performance bottlenecks, integration failures. |

External Risks | Factors outside the control of the project team. | Regulatory changes, supply chain disruptions, market shifts. |

Organizational Risks | Risks stemming from internal company processes or resources. | Funding cuts, staff turnover, poor communication channels. |

Project Management Risks | Risks related to the planning and execution of the project. | Unrealistic timelines, scope creep, inadequate resource allocation. |

🔍 Step 1: Risk Identification

The first step is to identify what could go wrong. This process relies on collaboration and diverse perspectives. A single person rarely sees all potential threats.

Techniques for Identification

Brainstorming Sessions: Gather the team and stakeholders to list potential risks. Encourage open discussion without immediate judgment.

SWOT Analysis: Review Strengths, Weaknesses, Opportunities, and Threats. This provides a structured view of internal and external factors.

Delphi Technique: Use anonymous surveys with experts to reach a consensus on risks without groupthink bias.

Checklist Analysis: Use historical data from similar past projects to identify recurring risks.

Root Cause Analysis: Ask “why” repeatedly to find the underlying causes of potential problems.

Documenting Risks

Once identified, risks must be recorded in a Risk Register. This document serves as the central source of truth for risk tracking. It should include:

Risk ID (Unique identifier)

Description of the risk

Category

Probability (Likelihood of occurrence)

Impact (Severity if it occurs)

Risk Owner (Person responsible for monitoring)

📊 Step 2: Risk Analysis and Prioritization

Not all risks are equal. Some are minor inconveniences, while others can terminate a project. You must analyze and prioritize them to allocate resources effectively.

Qualitative Risk Analysis

This method assesses the probability and impact of each risk using subjective scales. It is the most common approach due to its speed and ease of use.

Probability: Rated as Low, Medium, or High.

Impact: Rated as Low, Medium, or High.

Risk Score: Calculated by multiplying Probability by Impact.

This scoring helps distinguish between high-priority risks that require immediate attention and low-priority risks that can be monitored.

Quantitative Risk Analysis

For complex projects, qualitative methods may not be sufficient. Quantitative analysis uses numerical data to calculate the overall effect of risks on project objectives.

Monte Carlo Simulation: Uses computer models to predict the probability of different outcomes based on various risk scenarios.

Decision Tree Analysis: Maps out different decision paths and their associated probabilities to determine the best course of action.

Expected Monetary Value (EMV): Calculates the average outcome when the future includes scenarios that may or may not happen.

The Risk Matrix

A Risk Matrix visualizes the priority of risks based on probability and impact. It helps stakeholders quickly understand which risks demand resources.

Impact ↓ / Probability → | Low | Medium | High |

|---|---|---|---|

High | Medium Priority | High Priority | Critical |

Medium | Low Priority | Medium Priority | High Priority |

Low | Low Priority | Low Priority | Medium Priority |

🛠️ Step 3: Developing Response Strategies

Once risks are prioritized, you must decide how to handle them. The strategy depends on whether the risk is a threat or an opportunity.

Strategies for Threats

Avoid: Change the project plan to eliminate the risk entirely. For example, removing a feature that uses unstable technology.

Mitigate: Reduce the probability or impact of the risk to an acceptable threshold. This involves taking proactive steps to reduce the likelihood of occurrence.

Transfer: Shift the risk to a third party. Common methods include insurance or outsourcing specific tasks to vendors with more expertise.

Accept: Acknowledge the risk but take no action unless it occurs. This is suitable for low-priority risks where the cost of mitigation exceeds the potential loss.

Strategies for Opportunities

Exploit: Ensure the opportunity definitely happens. This is the opposite of avoiding a threat.

Enhance: Increase the probability or impact of the opportunity to maximize benefits.

Share: Allocate ownership of the opportunity to a third party who can best capture it.

Accept: Be willing to take advantage if the opportunity arises, but do not actively pursue it.

👀 Step 4: Monitoring and Controlling Risks

Risk management is not a one-time activity. It occurs throughout the project lifecycle. Risks change, new risks emerge, and old risks may disappear.

Key Activities

Track Identified Risks: Regularly review the risk register to update status and ensure owners are active.

Identify New Risks: Continuously scan for emerging threats during status meetings and milestone reviews.

Monitor Triggers: Watch for warning signs that indicate a risk is about to occur.

Evaluate Risk Effectiveness: Determine if the response strategies are working or if adjustments are needed.

Risk Audits: Periodically review the risk management process to ensure it remains effective.

Communication Plans

Stakeholders need to know about significant risks. A communication plan defines who gets informed, when, and how. This ensures transparency without causing unnecessary alarm.

High-Priority Risks: Report immediately to senior management.

Medium-Priority Risks: Include in weekly status reports.

Low-Priority Risks: Review during monthly steering committee meetings.

⚠️ Common Pitfalls in Risk Assessment

Even experienced teams make mistakes. Being aware of common errors helps you avoid them.

Optimism Bias: Assuming everything will go smoothly. This leads to underestimating costs and time.

Confirmation Bias: Only looking for risks that support a preferred outcome while ignoring negative indicators.

Analysis Paralysis: Spending too much time analyzing risks and not enough time acting on them.

Ignoring Soft Risks: Focusing only on technical issues and ignoring team morale or stakeholder engagement.

Static Registers: Treating the risk register as a document to be created once, rather than a living tool.

🤝 Fostering a Risk-Aware Culture

The best tools and processes fail if the team culture discourages reporting problems. Employees must feel safe to raise concerns without fear of retribution.

Encourage Open Dialogue: Make it clear that identifying risks is a positive contribution, not a criticism.

Lead by Example: Leaders should admit their own uncertainties and discuss how they manage them.

Reward Early Warnings: Recognize team members who identify issues before they become problems.

Training: Provide training on risk management principles to all team members, not just project managers.

🔄 Post-Project Review and Lessons Learned

The project lifecycle ends with a review. This phase is crucial for improving future risk management.

Review Risk Outcomes: Did the predicted risks occur? Did the mitigation strategies work?

Update Checklists: Add new risks to the organizational knowledge base for future projects.

Document Successes: Note which risks turned into opportunities and how they were handled.

Celebrate Resilience: Acknowledge the team’s ability to navigate challenges successfully.

📝 Final Thoughts

Managing project risk is about balance. It requires vigilance without creating a culture of fear. By implementing structured identification, analysis, and response processes, you build resilience into your projects. This approach ensures that when unexpected events arise, your team is prepared to respond effectively, keeping the project on track.

Start by updating your risk register today. Engage your team in a brainstorming session. Small steps now prevent major disruptions later. Remember, the goal is not to eliminate all uncertainty, but to manage it with competence and foresight.